Contents

Overview

The concept of a premium for bearing risk in financial markets predates formal academic study. Early pioneers like Benjamin Graham and David Dodd in their seminal work, "Security Analysis" (1934), implicitly acknowledged that investors required higher returns for riskier assets, though they didn't quantify it as a specific "equity risk premium." The modern understanding owes much to the work of Harry Markowitz, whose portfolio theory laid the groundwork for understanding risk and return trade-offs. Later, William Sharpe and John Lintner further developed the Capital Asset Pricing Model (CAPM), which explicitly incorporated the ERP as a key input for determining expected asset returns. The empirical validation and estimation of the ERP became a central focus for financial economists thereafter, with significant contributions from researchers like Richard Roll and Eugene Fama.

⚙️ How It Works

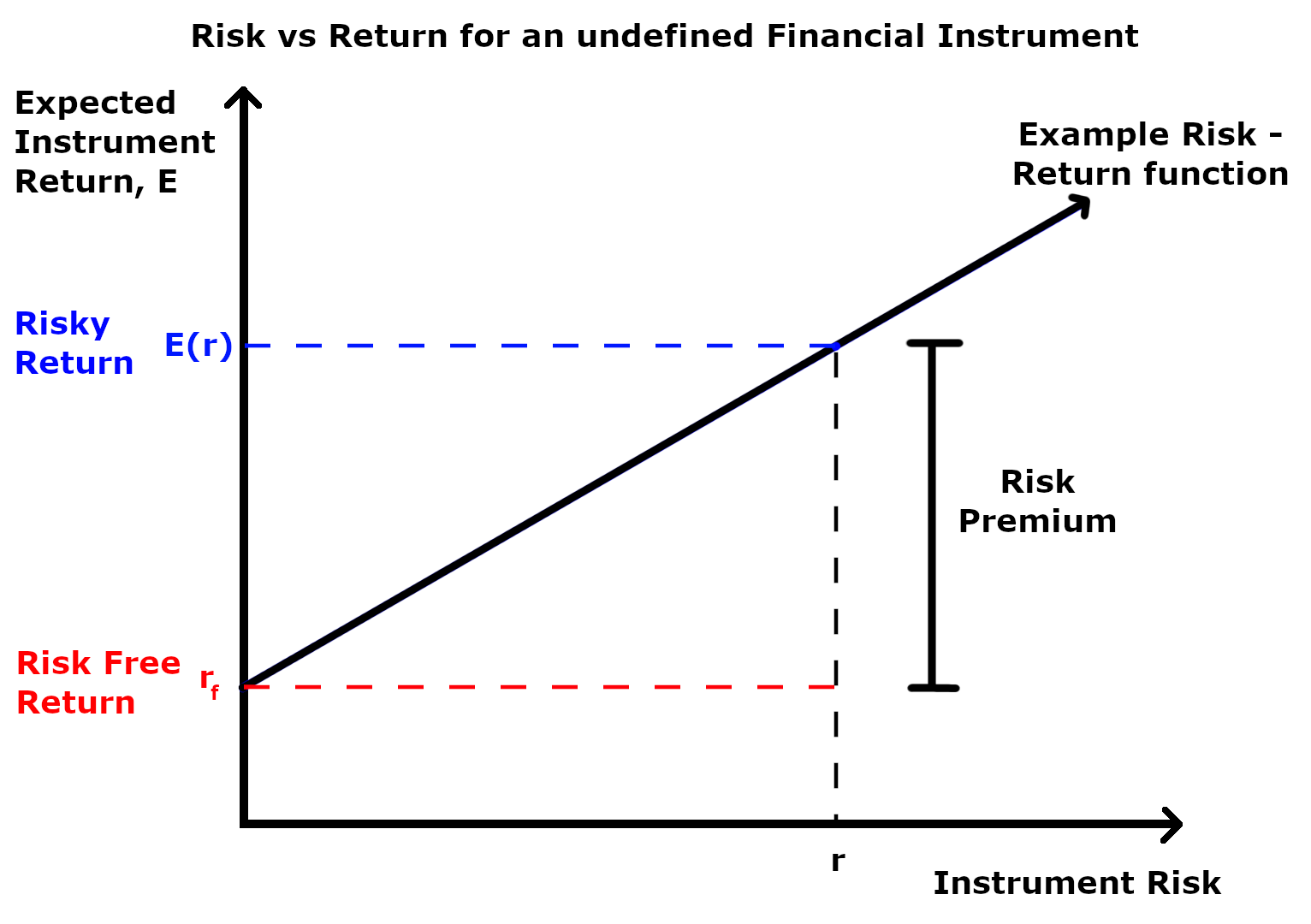

At its core, the equity risk premium is calculated as the expected return on a broad market index (like the S&P 500) minus the yield on a risk-free asset, typically a long-term government bond such as U.S. Treasury bonds. The formula is often expressed as E(R_equity) - R_f, where E(R_equity) is the expected return on equities and R_f is the risk-free rate. The "expected" part is critical and contentious; it's not a historical average but a forward-looking estimate. This expectation is influenced by factors like current market valuations, economic growth prospects, inflation expectations, and investor sentiment. Different models, such as dividend discount models or earnings yield models, are employed to forecast future equity returns, each with its own set of assumptions and potential biases. The risk-free rate itself is also subject to interpretation, with debates over whether to use short-term or long-term yields.

📊 Key Facts & Numbers

Estimates for the historical ERP vary significantly. Global ERPs can differ substantially; emerging markets typically demand higher premiums due to greater political and economic instability. The volatility of the ERP is also notable; it can shrink dramatically during market booms and expand during crises. For example, during the dot-com bubble of the late 1990s, valuations soared, implying a lower ERP, while the 2008 financial crisis saw a surge in perceived risk, widening the premium. The average inflation rate over the period also plays a role, with higher inflation often correlating with higher nominal risk-free rates and, consequently, potentially higher nominal ERPs.

👥 Key People & Organizations

Key figures in the development and ongoing study of the ERP include Harry Markowitz, whose portfolio theory provided the theoretical foundation for risk-return analysis. William Sharpe and John Lintner were instrumental in formalizing the CAPM, which hinges on the ERP. Benjamin Graham, the father of value investing, emphasized risk aversion and margin of safety, concepts intrinsically linked to the ERP. Academics like Aswath Damodaran at NYU Stern continuously publish updated estimates of ERPs for various global markets. Major financial institutions like Goldman Sachs and J.P. Morgan regularly publish their own ERP estimates for institutional clients, influencing market expectations. Organizations such as S&P Dow Jones Indices provide data that underpins many historical ERP calculations.

🌍 Cultural Impact & Influence

The ERP has profoundly shaped modern finance, serving as a bedrock for asset pricing, portfolio construction, and corporate finance decisions. It underpins the logic of value investing, where investors seek undervalued securities that offer a substantial margin of safety against potential downturns. The concept is embedded in the discounted cash flow (DCF) model, a ubiquitous tool for valuing companies, where the ERP is a key component of the discount rate. Its influence extends to retirement planning, as financial advisors use ERP estimates to project long-term portfolio growth for clients saving for retirement. The widespread adoption of CAPM and similar models in academic and professional circles means that the ERP is implicitly or explicitly considered in investment decisions globally, influencing capital allocation across industries and geographies.

⚡ Current State & Latest Developments

In the current investment climate, the ERP remains a focal point of discussion amidst elevated interest rates and ongoing geopolitical uncertainties. Some analysts observe that persistently high inflation and central bank tightening cycles have increased the risk-free rate significantly, potentially compressing the nominal ERP. Others argue that heightened recession fears and market volatility justify a higher ERP. For instance, the Federal Reserve's aggressive rate hikes in 2022-2023 have reshaped the risk-free landscape, prompting re-evaluation of equity valuations. Furthermore, the rise of AI and its potential to disrupt industries is introducing new layers of uncertainty, complicating forward-looking ERP estimates. Discussions often revolve around whether current market prices adequately reflect these evolving risks.

🤔 Controversies & Debates

The primary controversy surrounding the ERP is its estimability. Critics argue that relying on historical data to predict future returns is flawed, as market conditions, investor behavior, and economic structures change over time. The "forward-looking" nature of the ERP means it's based on subjective forecasts, leading to a wide dispersion of estimates among experts. The ERP is not a constant but fluctuates significantly, making it a poor predictor of actual future returns. Another debate centers on the appropriate risk-free rate to use—should it be the yield on short-term government bills or long-term bonds? The choice can materially alter the calculated premium. Furthermore, the concept of a single "market" ERP is challenged by the fact that different asset classes and individual stocks have vastly different risk profiles.

🔮 Future Outlook & Predictions

The future of the equity risk premium will likely be shaped by several macro trends. Persistent inflation or a potential stagflationary environment could keep risk-free rates elevated, potentially suppressing the ERP unless equity earnings growth accelerates dramatically. The ongoing energy transition and technological disruption (e.g., quantum computing) introduce new sources of risk and opportunity, potentially leading to higher ERPs for certain sectors or markets. As global economic integration continues, the interconnectedness of markets may lead to more synchronized movements in ERPs worldwide, though regional divergences will persist. Some futurists predict that as demographics shift and more passive investing becomes the norm, the ERP might naturally decline due to reduced demand for active risk-taking, while others foresee increased volatility from climate change and geopolitical risks pushing it higher.

💡 Practical Applications

The ERP is a critical input for numerous practical applications in finance. For individual investors, it helps frame expectations for long-term stock market returns, guiding asset allocation decisions between stocks and bonds. In corporate finance, it's a key component of the Weighted Average Cost of Capital (WACC), used to discount future cash flows and evaluate the profitability of potential projects and investments. Investment banks and asset managers use ERP estimates to value companies, determine target stock prices, and construct portfolios designed to meet specific risk-return objectives. For example, a company considering a new factory might use an ERP estimate to calculate the required rate of return for that investment, ensuring

Key Facts

- Category

- finance

- Type

- topic